U.S. Produced Water Treatment Market: Treatment Technology (Physical Treatment, Chemical Treatment, Biological Treatment); Produced Water Usage (Agricultural Use, Industrial Use, Municipal Use, Oil & Gas Field Operations, Other Emerging Uses); Application (Onshore Operations and Offshore Operations); Sources of Produced Water (Conventional Sources and Unconventional Sources); End User (Oil & Gas Operators (Upstream, Offshore, Onshore), Midstream & Water Services Companies, Independent Water Treatment Service Providers, Power Generation Facilities, Mining & Mineral Processing Companies, Chemical & Petrochemical Industries, Municipal & Regional Water Authorities)—Market Size, Industry Dynamics, Opportunity Analysis and Forecast for 2025–2033

- Last Updated: 30-Sep-2025 | | Report ID: AA09251518

Market Scenario

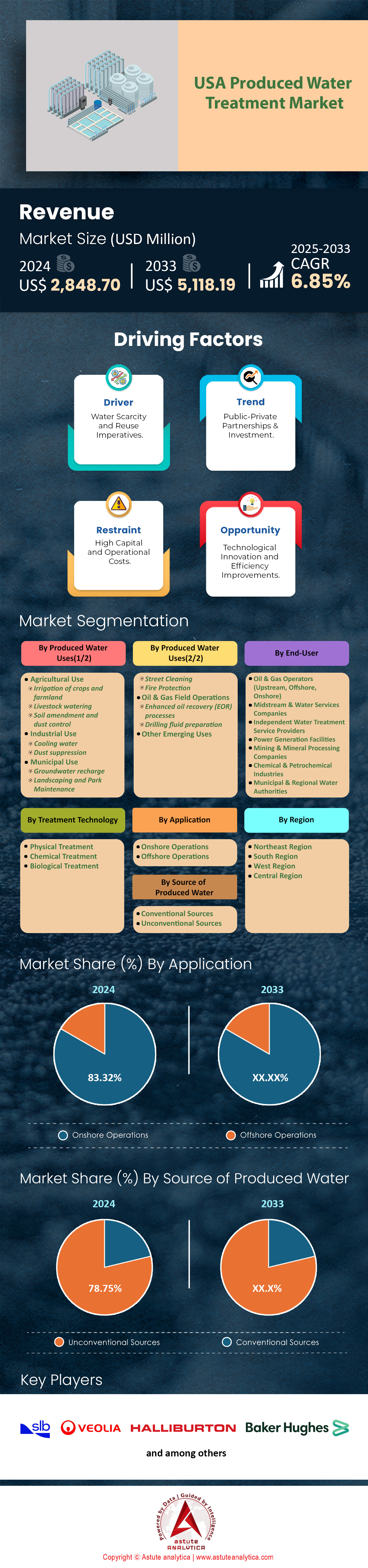

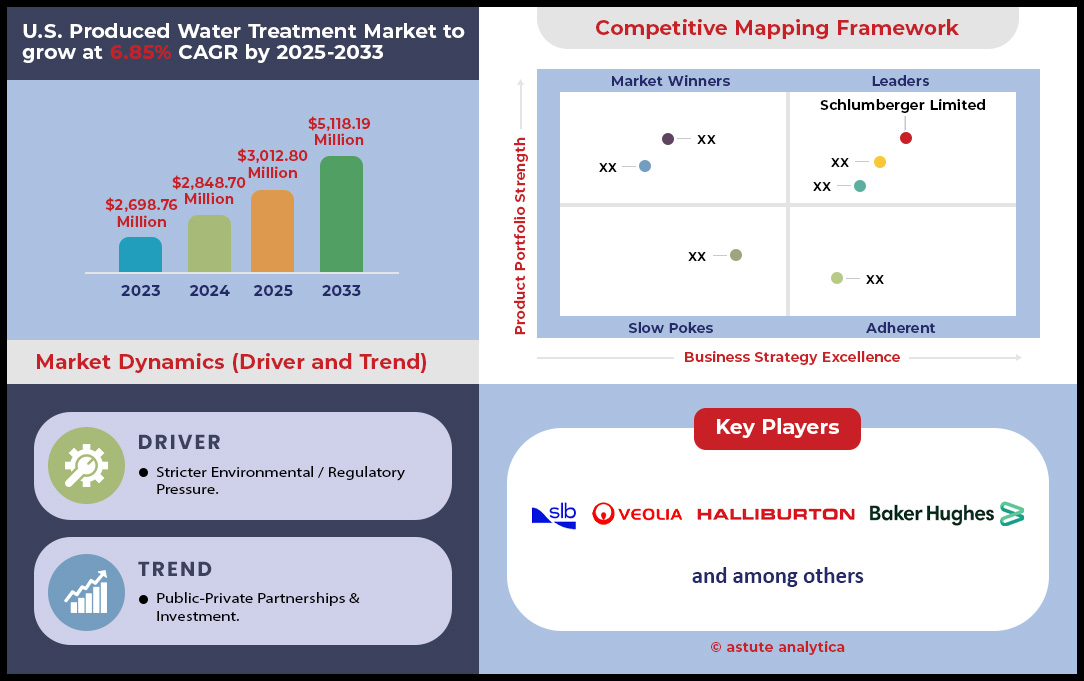

U.S. produced water treatment market was valued at US$ 2,848.70 million in 2024 and is projected to hit the market valuation of US$ 5,118.19 million by 2033 at a CAGR of 6.85% during the forecast period 2025–2033.

Key Findings in United States Produced Water Treatment Market

- Based on treatment technology, physical treatment firmly positions itself at the forefront with revenue share of 47.70% of the US produced water treatment market.

- Based on produced water uses, oil & gas field operations are generating more than 67.14% market revenue.

- Based on application, Onshore Operations accounts for 83.32% share of the US market.

- Based on sources of produced water, unconventional sources take up the largest share of over 78.75% market share.

- US produced water treatment market is set to grow at robust CAGR of 6.85% during the forecast period 2025-2033.

The demand trajectory for the U.S. produced water treatment market is shaped by three powerful and interconnected forces. Foremost among them, staggering production volumes set a fundamental and uncompromising requirement for extensive treatment services. The Permian Basin alone generates immense quantities of produced water, with major operators like Chevron producing over 20 million barrels daily as of 2025. The combined output from the Delaware and Midland sub-basins is approximately 11 million barrels per day. Intensifying this volume challenge are escalating water-to-oil ratios, which in some Permian wells reach as high as twelve to one, directly multiplying the treatment demand for each barrel of oil produced.

A tightening regulatory landscape, driven by environmental concerns like seismicity, is forcing a strategic pivot away from traditional disposal in the United States produced water treatment market. In a single week of July 2024, West Texas experienced 121 earthquakes, prompting regulators to act. In early 2024, Texas authorities suspended 23 disposal well permits, and new guidelines effective June 1, 2025, will further restrict injection activities. Oklahoma's new directives apply to 347 disposal wells, fundamentally altering water management practices and creating urgent demand for alternative solutions like advanced treatment and recycling.

At last, compelling economic drivers are accelerating the shift from viewing produced water as waste to a valuable resource. With disposal fees reaching $1.00 per barrel and trucking costs at $2.50 per barrel, water recycling offers dramatic savings of up to $2.50 per barrel on operating expenses. This economic reality, coupled with massive new contracts like Veolia’s $550 million deal for a single treatment facility, showcases a market where investment in treatment technology is no longer optional but a core component of profitable and sustainable energy production.

To Get more Insights, Request A Free Sample

Untapped Revenue Streams Transform the Produced Water Value Proposition

- Produced Water as a Critical Mineral Source: A paradigm shift is underway as companies in the United States produced water treatment market begin to view oilfield brine not as waste, but as a domestic source for critical minerals like lithium. Direct Lithium Extraction (DLE) technologies are turning produced water into a strategic asset for the U.S. battery supply chain. Volt Lithium scaled its Permian Basin DLE operations to over 11,000 barrels per day in early 2025. Research from the National Energy Technology Laboratory suggests wastewater from the Marcellus Shale alone could potentially meet 38–40% of current U.S. lithium demand. With approximately 20 million barrels of lithium-rich water produced daily in the Permian, the economic incentive to mine this "liquid gold" is creating a powerful new demand driver for specialized treatment solutions.

- Federally-Funded Expansion into Non-Oilfield Reuse: Driven by acute water scarcity in the American West, significant federal and state funding is now fueling research into treating produced water for beneficial reuse outside the oilfield, particularly in agriculture and industry. In January 2025, the Department of the Interior announced $223 million for water recycling and desalination projects. Furthermore, the Department of Energy allocated nearly $8 million in April 2024 for five new R&D projects focused on produced water management. States like New Mexico are running multiple pilot programs, with one state plan aiming to unlock 100,000 acre-feet of new water by 2028, creating a government-supported pathway for market expansion.

Direct Lithium Extraction Creates an Unprecedented Economic Demand Driver

The quest for domestic lithium supply is fundamentally reshaping demand within the US produced water treatment market. The focus is rapidly shifting from mere water disposal to sophisticated mineral extraction, creating a lucrative new vertical. This is driven by massive project scale-ups and compelling economics. For instance, Volt Lithium's Generation 5 Field Unit, deployed in January 2025, immediately surpassed its 10,000 barrels per day (bpd) target. The company’s operations astonishingly scaled from 600 bpd to over 11,000 bpd in just six months. Such rapid expansion is a response to a tightening global market, where the projected lithium surplus is expected to shrink from 150,000 tons in 2024 to 80,000 tons in 2025, with a potential deficit of 1,500 tons emerging as early as 2026.

Major investments confirm the long-term viability of this demand driver. The Thacker Pass project carries an estimated capital expenditure of US$2.3 billion, aiming for an annual capacity of 40,000 tons of lithium carbonate. Similarly, American Lithium's TLC Project has a Phase 2 goal of 48,000 tons annually. Established players are also expanding; Albemarle is boosting its brine production to 7,500 tons per year by 2025, supported by 22 new production wells capable of pumping 20,000 acre-feet of brine. The potential to offset significant disposal costs, such as the $21 million spent by COG Operating over a two-year period, further solidifies produced water mining as a primary market force.

Targeted Government Investment and Regulation Accelerate Market Adoption

Federal and state initiatives are injecting significant capital and creating a stable regulatory framework in the produced water treatment market, directly fueling demand for innovative water treatment technologies. On January 14, 2025, the Department of the Interior announced a landmark $223 million for water recycling projects. A large portion of these funds originates from the Bipartisan Infrastructure Law, which allocates a total of $8.3 billion over five years for water projects and has already directed almost $5.3 billion to more than 670 projects. The Department of Energy is also a key player, announcing nearly $8 million for five R&D projects on April 18, 2024, part of a broader $18,050,000 funding opportunity for water R&D.

State-level actions provide further market certainty. New Mexico’s ambitious plan aims to unlock 100,000 acre-feet of new water for industrial use by 2028, creating a clear target for technology developers. These programs are supported by dedicated research funding. The Bureau of Reclamation offered up to $2 million for proposals due November 13, 2024, while the USGS posted its fiscal year 2025 funding opportunities with deadlines in September 2025. Even early-stage regulatory drafts, such as a New Mexico proposal to allow pilot projects to release up to 84,000 gallons of treated water daily, signal a clear government-led pathway toward broader adoption of advanced solutions in the US produced water treatment market.

Segmental Analysis

Physical Treatment's Cost-Effective Dominance in Produced Water Management

Physical treatment technologies command a substantial 47.70% of the US produced water treatment market due to their cost-effectiveness and high efficiency in the crucial primary stages of water treatment. These methods, including gravity separators, hydrocyclones, and filtration systems, are adept at removing suspended solids and dispersed oil, which are the most common contaminants in produced water. Their operational simplicity and reliability make them the foundational step in most treatment processes, preparing the water for more advanced secondary and tertiary treatments if required. The lower operational expenditure associated with physical treatment compared to more complex technologies like membrane or chemical treatments further solidifies its leading position, especially given the vast volumes of water that need to be managed daily in the oil and gas sector.

In the competitive landscape of the US produced water treatment market, physical treatment's leading position is reinforced by strong operational metrics. The cost of reusing water, often starting with physical treatment, is between $0.15 to $0.20 per barrel, making it more economical than disposal costs which can be as high as $1 per barrel. Offshore facilities in the Gulf of Mexico are mandated to limit the oil content in discharged water to a monthly average of 29 ppm, a target often achieved through efficient physical separation. For 2025, systems with a capacity of 100-500 thousand barrels per day are expected to be the most widely deployed, underscoring the need for high-volume physical treatment solutions. The total government revenues from UK oil and gas production, an indicator of the scale of operations that generate produced water, surged to $1.84 billion in the 2021-2022 tax year, a significant increase from $0.39 billion the previous year.

- Hydrocyclones, a key physical treatment technology, are utilized in approximately 90% of offshore produced water treatment facilities.

- Recent advancements in hydrocyclone design have led to separation efficiencies of up to 67.6% for certain inlet oil concentrations.

- The life cycle water consumption for a Marcellus shale gas well can have a freshwater ecotoxicity potential of between 900 and 23,000 kg of 2,4D-equivalent if the produced water is not adequately treated, highlighting the critical role of primary physical treatment.

Oil & Gas Operations Driving Revenue in Produced Water Reuse

Oil & gas field operations generate more than 67.14% revenue of the produced water treatment market from produced water uses primarily because of the immense water requirements for hydraulic fracturing. Reusing produced water within the oilfield is a significantly more cost-effective and logistically efficient solution than sourcing freshwater, especially in the water-scarce regions where many prolific shale plays are located. The reuse of produced water minimizes the costs associated with freshwater acquisition and transportation, as well as the expenses and regulatory hurdles of produced water disposal. As drilling and completion activities continue to demand large volumes of water, the economic and environmental benefits of a closed-loop water management system within oil and gas operations are compelling, driving the high market revenue share.

The financial and operational incentives for reusing produced water within the oil and gas sector are substantial. In Texas, an estimated 33 million barrels of produced water are generated daily. Reusing this water for hydraulic fracturing, where a single well can require an average of 14.3 million gallons, presents a massive opportunity for cost savings. The Permian Basin alone is projected to generate 22.3 million barrels of produced water per day in 2025, further emphasizing the scale of this resource. In 2024, one water solutions company recycled over 280 million barrels of produced water in the Permian Basin, showcasing the significant volumes being managed. The US produced water treatment market is capitalizing on this trend, with companies offering innovative solutions for in-field reuse.

- A single-day supply record of 500,000 barrels of recycled produced water was achieved by one company in New Mexico, demonstrating the high capacity of modern recycling facilities.

- It is estimated that by 2030, the amount of fresh and brackish water used in Permian completions will be 500,000 barrels per day less than in 2017, thanks to increased recycling.

- The development of salt-tolerant fracturing fluids has been a major technological enabler for the increased reuse of produced water with high TDS levels.

Unconventional Sources Fueling Produced Water Treatment Demand

Unconventional sources, such as shale gas and tight oil, contribute the largest share of over 78.75% of United States produced water treatment market due to the water-intensive nature of hydraulic fracturing. Unlike conventional wells, unconventional wells require millions of gallons of water for the initial fracturing process, a significant portion of which returns as flowback water. Furthermore, over the lifetime of these wells, they tend to produce a higher ratio of water to hydrocarbons compared to many conventional wells. The rapid development and widespread adoption of horizontal drilling and multi-stage hydraulic fracturing across major US shale basins have unlocked vast energy resources, and in doing so, have generated an unprecedented and sustained volume of produced water that requires management.

The characteristics of unconventional produced water drive the produced water treatment market dynamics. In the Permian Basin, the average water cut is higher than in any other unconventional play, with three to four barrels of water produced for every barrel of oil. The produced water from shale formations like the Marcellus can have very high Total Dissolved Solids (TDS) concentrations, ranging from 40,000 to over 120,000 mg/L, necessitating specialized treatment solutions. The cost to treat this high-TDS water can be substantial, with thermal desalination estimated at 53-71 per cubic meter. The US fracking water treatment market was valued at approximately $165.6 million in 2024 and is projected to grow, driven by these large water volumes.

- Produced water from the Bakken shale has a median TDS of 244 g/L, which is about seven times that of seawater.

- The development of Marcellus shale increased the total oil- and gas-associated wastewater in Pennsylvania by an estimated 570% since 2004.

- The volume of water used for hydraulic fracturing in the Permian Basin is projected to be nearly four times less than the volume of produced water generated, creating a significant surplus that requires management. Recent Developments in United States Produced Water Treatment Market

Customize This Report + Validate with an Expert

Access only the sections you need—region-specific, company-level, or by use-case.

Includes a free consultation with a domain expert to help guide your decision.

Onshore Operations The Uncontested Leader in Produced Water Generation

Onshore operations account for a commanding 83.32% share of the US produced water treatment market, a direct reflection of the onshore focus of the nation's oil and gas production, particularly from unconventional shale plays. The sheer number of wells and the volume of hydrocarbons extracted from onshore basins like the Permian, Eagle Ford, and Bakken result in the generation of vast quantities of produced water. In contrast, offshore production, while significant, involves a smaller number of wells and a more contained operational footprint. The logistical ease and lower costs of developing and operating water treatment and disposal infrastructure on land, compared to the complexities of offshore environments, further contribute to the dominance of the onshore segment in the US produced water treatment market.

The scale of onshore activities underpins its market leadership. In 2023, U.S. oil output reached 12.9 million barrels per day, largely driven by onshore shale production. In the Permian Basin, the water-to-oil ratio can be as high as twelve to one, meaning significantly more water than oil is produced. The total water managed in the Permian soared from 6.3 million barrels a day in 2017 to 18.9 million barrels per day in 2023. This massive volume necessitates a robust onshore infrastructure for the US produced water treatment market. In Texas alone, a historic $20 billion investment in water infrastructure has been approved, with a portion expected to support produced water management solutions.

- The Texas legislature has established a fund that will dedicate $1 billion annually for the next 20 years to water infrastructure projects.

- There are approximately 144,000 Class II injection wells in the United States for the disposal of produced water, the vast majority of which are onshore.

- The cost of trucking produced water for disposal can be a significant operational expense for onshore producers, driving the adoption of localized treatment and reuse.

To Understand More About this Research: Request A Free Sample

Strategic Investments Reshaping US Produced Water Treatment Market Landscape

- Federal Funding Boost: In a significant move, the U.S. Department of

Energy announced nearly $8 million in April 2024 for five R&D

projects focused on produced water treatment and management. This is part of a larger $18 million funding opportunity to develop technologies for beneficial end-uses. - Strategic Acquisition for Expansion: SLB revealed its agreement to

acquire ChampionX Corporation in April 2024. This acquisition is set to

significantly broaden SLB's capabilities in chemical solutions and

produced water management. - Midstream Consolidation: Energy Transfer completed its acquisition of WTG Midstream in July 2024 for $2.275 billion. Concurrently, it entered into a joint venture with Sunoco LP, consolidating crude oil and produced water assets in the Permian Basin.

- Technology-Focused Investment: VVater, a next-generation water

treatment company, secured a multi-million dollar funding round in December 2024. The investment, backed by prominent figures like Tim Draper, will drive the expansion of its innovative chemical-free purification technology. - Targeted Infrastructure Growth: In October 2024, Enterprise Products

Partners acquired Piñon Midstream for $950 million. This move adds crucial gathering pipelines, treatment facilities, and disposal wells to its

Permian Basin assets in the United States produced water treatment market. - Advanced Technology Launch: Demonstrating a commitment to innovation, Adaptive Process Solutions launched its Microbubble Infusion Unit in January 2024. This system is designed to optimize contaminant removal in produced water, enhancing treatment efficiency.

- Government Grants for Water Efficiency: The Bureau of Reclamation

continues to fund water efficiency projects through its WaterSMART program. Multiple application rounds for grants were held throughout 2024, with another deadline set for January 2025, encouraging sustainable water use.

Top Companies in the U.S. Produced Water Treatment Market

- Halliburton Company

- Enviro-Tech Systems

- Weatherford International

- NOV

- Mineral Technologies, Inc.

- Baker Hughes

- TechnipFMC pic

- Ovivo

- Schlumberger Limited

- Cannon Artes S.p.A.

- Veolia Environnement S.A.

- Other Prominent Players

Market Segmentation Overview

By Treatment Technology

- Physical Treatment

- Chemical Treatment

- Biological Treatment

By Produced Water Uses

- Agricultural Use

- Irrigation of crops and farmland

- Livestock watering

- Soil amendment and dust control

- Industrial Use

- Cooling water

- Dust suppression

- Municipal Use

- Groundwater recharge

- Landscaping and Park Maintenance

- Street Cleaning

- Fire Protection

- Oil & Gas Field Operations

- Enhanced oil recovery (EOR) processes

- Drilling fluid preparation

- Other Emerging Uses

By Application

- Onshore Operations

- Offshore Operations

By Source of Produced Water

- Conventional Sources

- Unconventional Sources

By End User

- Oil & Gas Operators (Upstream, Offshore, Onshore)

- Midstream & Water Services Companies

- Independent Water Treatment Service Providers

- Power Generation Facilities

- Mining & Mineral Processing Companies

- Chemical & Petrochemical Industries

- Municipal & Regional Water Authorities

By Region

- Northeast Region

- Pennsylvania

- New York

- Ohio

- West Virginia

- New Jersey

- South Region

- Texas

- Louisiana

- Oklahoma

- Arkansas

- West Region

- California

- Colorado

- Wyoming

- New Mexico

- Alaska

- Central Region

- Dakota

- Montana

- Kansas

- Nebraska

- Minnesota

LOOKING FOR COMPREHENSIVE MARKET KNOWLEDGE? ENGAGE OUR EXPERT SPECIALISTS.

SPEAK TO AN ANALYST

.svg)

Features | Type of License | ||||

Data Book | Single User |   Multi User | Corporate | ||

| e-Access | ✓ | ✓ | ✓ | ✓ | |

User Sharing | 1 User Only | 1 User Only | Up to 7 Users | Unlimited User Access | |

⨉ | ⨉ | ⨉ | ✓ | ||

Free Customization | No Free Customization | Up To 30 hrs work | Up To 60 hrs work | Up To 80 hrs work | |

Deliverable |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analyst Support | 2-Months Analyst Support | 4-Months Analyst Support | 7-Months Analyst Support | One Year Analyst Support | |

Free Report update in next update cycle | ⨉ | ⨉ | ⨉ | ✓ | |

Free Industry Update (Within 180 days) | ⨉ | ⨉ | ⨉ | ✓ | |

Benefit | Up to 10% off on Post Purchase | Up to 20% off on Post Purchase | Up to 30% off on Post Purchase | Up to 40% off on Post Purchase | |